For banks and credit unions, finding ways to grow lending portfolios while keeping risk manageable is always a top priority. The Small Business Administration or SBA 504 loan program offers a unique opportunity to do both. By partnering with a Certified Development Company (CDC) such as Statewide CDC, lenders can provide small businesses with affordable, long-term financing while maintaining a secure lending position and reducing overall exposure.

SBA 504 loans are designed for commercial real estate and equipment purchases, combining private-sector lending with government backing. In result, this unique structure benefits the borrowers with stability and lower rates and provides lenders stronger portfolios, more approvals, and lower risk on every qualified project.

Why Lenders Should Consider SBA 504 Loans

Partnering with a CDC like Statewide CDC allows lenders to access a proven program that fuels small business growth while strengthening their own lending performance. Here are the key advantages:

Reduced Lender Risk

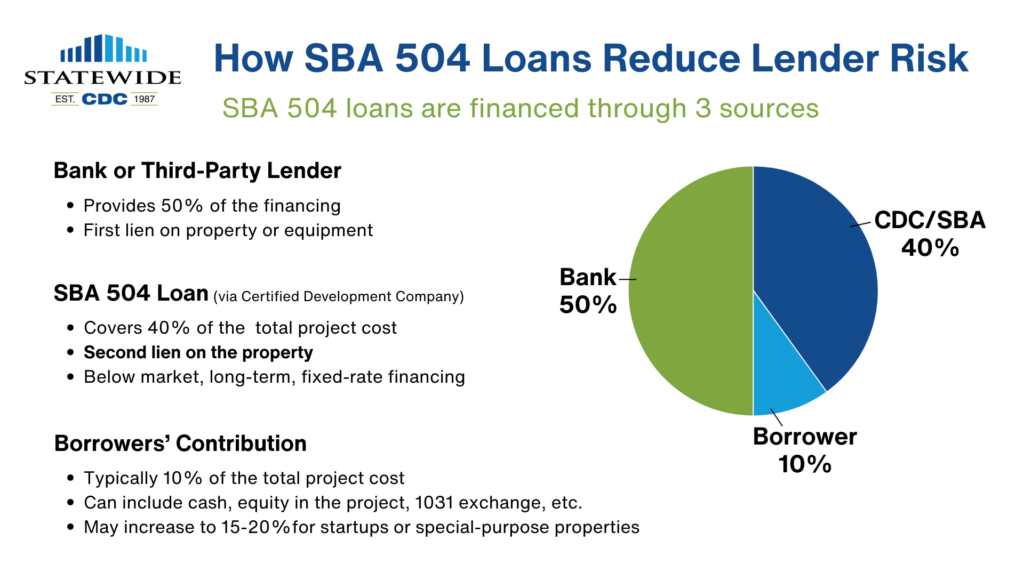

Under the 504 structure, the bank typically finances 50 percent of the total project, while the SBA-backed CDC covers 40 percent and the borrower contributes the remaining 10 percent. This means the lender’s exposure is limited to half of the project cost, even though they hold the first lien position. The SBA guarantee on the CDC portion further stabilizes the overall financing package, greatly minimizing default risk.

More Loan Opportunities

The SBA 504 program gives lenders the ability to finance owner-occupied commercial real estate, construction, and major equipment purchases with long-term, fixed-rate stability. In turn, it makes it easier for banks and credit unions to say “yes” to more borrowers who might otherwise struggle to qualify for conventional financing.

Higher Loan Approval Rates

Because borrowers only need to contribute 10 percent equity, more businesses can meet the requirements for a 504 project. This expands the lender’s pool of qualified applicants, supporting growth in both loan volume and community impact.

Portfolio Growth with Security

Lenders maintain senior lien position on their portion of the loan, ensuring security while the SBA and CDC share the remainder of the project financing. This structure encourages portfolio expansion with reduced default risk and predictable returns.

How Statewide CDC Supports Lenders

At Statewide CDC, our goal is to make SBA lending simple, fast, and beneficial for every partner institution. We provide direct support throughout the loan process so lenders can focus on serving their clients.

Expert Loan Structuring

Our team manages all aspects of SBA 504 compliance and packaging. We structure each loan to meet SBA requirements, ensuring smooth approvals and faster funding.

Fast Prequalification

We provide no-cost borrower prequalification within 24 hours, giving lenders confidence in the borrower’s eligibility before proceeding. This quick turnaround helps lenders close more loans, more efficiently.

Ongoing Support

From initial underwriting to documentation and closing, our experienced SBA specialists assist lenders every step of the way. We coordinate with borrowers, appraisers, and SBA reviewers to keep the process on track and reduce administrative burden for your team.

Partnering with Statewide CDC means having a reliable ally that understands both the borrower’s needs and the lender’s priorities.

Why SBA 504 Lending Is a Win-Win

SBA 504 financing creates genuine value on both sides of the lending relationship. For lenders, it opens the door to steady portfolio growth backed by strong collateral and reduced exposure. For business owners, it provides affordable, long-term financing that makes expansion and ownership attainable. Beyond the individual transaction, every 504 project fuels community progress by creating jobs, strengthening local economies, and helping small businesses establish long-term stability.

Statewide CDC’s partnerships with banks and credit unions across California have helped fund hundreds of successful projects. By combining federal loan support with local expertise, we help lenders meet community lending goals while building stronger relationships with small business clients.

Get Started with Statewide CDC

If your institution is ready to expand its SBA lending opportunities, Statewide CDC can help. Our lender support team provides personalized assistance to ensure every project is structured efficiently and approved quickly. You can even schedule one of our lending experts to train your lending team and provide critical changes or updates to the SBA loan program.

Contact Statewide CDC today to learn more about becoming a 504 lending partner and discover how SBA financing can help you serve more clients while maintaining strong portfolio performance.

Frequently Asked Lender Questions

What makes SBA 504 loans attractive to lenders?

The 504 program reduces lender risk by limiting exposure to 50 percent of the total project cost while the SBA guarantees the CDC portion and provides below market interest rate that is fully amortized over 25 years.. Lenders maintain the first lien position, ensuring security on their investment.

How does partnering with a CDC benefit my institution?

A Certified Development Company like Statewide CDC handles the SBA compliance, packaging, and approval process. This saves time for your lending team and ensures that all projects meet program requirements.

Can SBA 504 loans help meet CRA or community lending goals?

Yes. The SBA 504 program directly supports local business growth and job creation, making it an effective way for lenders to fulfill Community Reinvestment Act objectives.

What types of projects qualify for SBA 504 financing?

Eligible projects include owner-occupied commercial real estate purchases, building expansions, land and construction projects, and large equipment acquisitions that promote business growth.

How quickly can a borrower be prequalified?

Statewide CDC can provide a prequalification letter within 24 hours of receiving complete financial documentation. This helps lenders move forward quickly with confidence.

Does the lender still handle underwriting?

Yes, lenders underwrite their 50 percent portion, while the CDC manages the SBA-backed portion. The two work together to create one seamless financing package for the borrower.

Is there a limit to how many 504 loans a lender can originate?

No. Many partner institutions close multiple SBA 504 loans each year, using the program as a reliable way to expand their small business lending portfolio.